SFIX's Client Experience Builds Path to Long-Term Profitability

Stitch Fix, Inc.’s SFIX emphasis on enhancing client experiences and maintaining a solid financial foundation, including a debt-free balance sheet, reinforces its potential for sustained profitability. The innovative use of AI and effective cost management positions the company for long-term success. As Stitch Fix continues its transformation and outlines a clear growth strategy, it is well-equipped to navigate the evolving retail landscape.

SFIX has demonstrated impressive performance by increasing its RPAC by 4.5% year over year, reaching $533 in the fourth quarter of fiscal 2024. This growth reflects the company’s effectiveness in deepening relationships with core clients through personalized and flexible shopping experiences.

By increasing the number of items in a "Fix," Stitch Fix has boosted average order values, leading to higher client spending. This rise in RPAC not only signifies successful product optimization but also indicates the potential for increased customer lifetime value, which is vital for long-term profitability.

Image Source: Zacks Investment Research

SFIX’s Innovations & Operational Efficiency Bode Well

Stitch Fix’s proprietary AI technology plays a pivotal role in delivering personalized client experiences at scale, with features like StyleFile contributing to a 5% rise in conversion rates among new clients. Despite revenue headwinds, the company has maintained profitability through cost control and operational optimization, achieving positive adjusted EBITDA for seven consecutive quarters.

In the fourth quarter, the adjusted EBITDA margin rose 90 basis points to 3%, while the gross margin expanded by 50 basis points year over year to 44.6%, driven by better inventory management and a focus on higher-margin private-label products.

The company implemented a cost-cutting initiative that saved more than $100 million in selling, general and administrative expenses in fiscal 2024. Looking forward, Stitch Fix anticipates additional savings in fiscal 2025 to enhance its bottom line. With a clear three-phase transformation strategy — rationalization, building and growth — the company aims to drive revenue growth by fiscal 2026.

Stitch Fix concluded the fiscal fourth quarter with $162.9 million in cash and no debt, providing the flexibility to invest in growth initiatives without financial burdens. This solid financial position, combined with its focus on innovation and client personalization, positions Stitch Fix favorably in a competitive retail landscape.

SFIX Stock’s Valuation Attractive

From a valuation perspective, the stock presents an attractive opportunity, trading at a discount relative to historical and industry benchmarks. With a forward 12-month price-to-sales ratio of 0.29, below the five-year median of 0.50 and the industry’s average of 1.14, the stock offers compelling value for investors seeking exposure to the sector. The stock currently has a Value Score of A, further validating its appeal.

Image Source: Zacks Investment Research

Estimate Revisions Favor Stitch Fix Stock

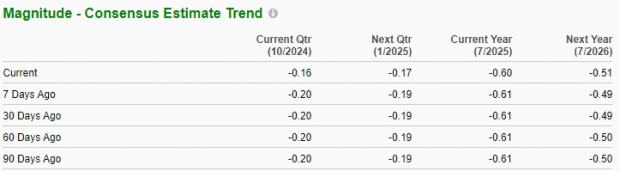

The Zacks Consensus Estimate for adjusted loss has been revised downward, reflecting the positive sentiment around Stitch Fix. Over the past seven days, analysts have decreased their adjusted loss estimates by 4 cents to 16 cents per share for the current quarter and by 2 cents to 17 cents for the next quarter. These estimates indicate year-over-year growth of 27.3% and 19.1%, respectively.

Image Source: Zacks Investment Research

SFIX’s Decreasing Active Client Base: A Major Hurdle

Stitch Fix faces a significant challenge with its declining active client base, which has been a primary contributor to the company’s revenue decrease over the past eight quarters. In the third quarter of fiscal 2024, the number of active clients fell to 2,633,000, marking a substantial 20% year-over-year decline.

As a result, the company experienced a revenue drop of 15.8% in the fiscal third quarter. This ongoing decline in sales points to persistent difficulties in client retention and acquisition, highlighting deeper issues related to product appeal or heightened competition in the market. Shares of the company have lost 28.6% in the past three months against the Zacks Retail - Apparel and Shoes industry’s 3.7% growth.

Wrapping Up

Investors may consider SFIX due to its strategic focus on enhancing client experiences and maintaining a solid financial foundation, including a debt-free balance sheet. The company has demonstrated the potential for sustained profitability through personalized shopping experiences and innovative use of AI, which has improved operational efficiency.

Despite challenges such as a declining active client base, the company’s commitment to innovation and growth positions it well in the evolving retail landscape. Stitch Fix currently carries a Zacks Rank #3 (Hold).

Stocks to Consider

Some better-ranked stocks are Nordstrom Inc. JWN, Abercrombie & Fitch Co. ANF and Crocs, Inc. CROX.

Nordstrom is a leading fashion specialty retailer in the United States. The company offers an extensive selection of both branded and private-label merchandise. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nordstrom’s fiscal 2024 sales indicates growth of 0.6% from the fiscal 2023 figure. JWN has a negative trailing four-quarter average earnings surprise of 17.8%.

Abercrombie is a specialty retailer of premium, high-quality casual apparel. It sports a Zacks Rank of 1 at present. ANF delivered a 16.8% earnings surprise in the last reported quarter.

The consensus estimate for Abercrombie’s fiscal 2025 earnings and sales indicates growth of 63.4% and 13.1%, respectively, from the fiscal 2024 reported levels. ANF has a trailing four-quarter average earnings surprise of 28%.

Crocs offers a wide variety of footwear products, including sandals, wedges, flips and slides that cater to people of all ages. It currently carries a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for Crocs’ 2024 earnings and sales indicates growth of 6.8% and 4%, respectively, from the 2023 reported figures. CROX has a trailing four-quarter average earnings surprise of 14.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Stitch Fix, Inc. (SFIX) : Free Stock Analysis Report