Insmed Stock Surges 168% in the Past Six Months: Here's Why

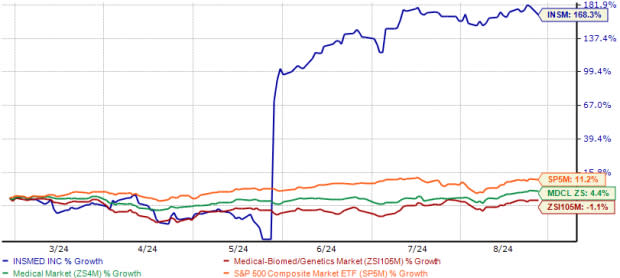

Shares of Insmed INSM have more than doubled in market value in the past six months against the industry’s 1.1% fall. During this timeframe, the stock has also outperformed the sector and the S&P 500.

The surge in stock price can be attributed to the company’s progress with its two pipeline candidates, brensocatib and treprostinil palmitil inhalation powder (TPIP), which are being developed in separate clinical studies targeting multiple lung disorders.

The company’s shares are also trading above the 50-day and 200-day moving averages.

Insmed’s Stock Outperforms Industry, Sector & S&P 500

Image Source: Zacks Investment Research

Let’s take a brief look at the factors that were responsible for this price jump.

Encouraging Bronchiectasis Development Aids INSM’s Prospects

Currently the most advanced candidate in Insmed’s pipeline, brensocatib was licensed from AstraZeneca AZN in 2016 as a potential treatment for multiple neutrophil-driven inflammatory conditions.

Earlier this May, Insmed reported positive topline results from the phase III ASPEN study, which evaluated brensocatib in patients withnon-cystic fibrosis bronchiectasis. The study met its primary endpoint — treatment with the drug achieved statistically significant and clinically meaningful reductions in the annualized rate of pulmonary exacerbations (or episodes of worsening disease symptoms) when compared with placebo.

Currently, there are no medications specifically approved to treat bronchiectasis. Per management estimates, nearly a million patients living in the United States, Europe and Japan are affected by the disease.

Based on the above results and target market size, Insmed expects to submit a regulatory filing for brensocatib in bronchiectasis in the fourth quarter of 2024. If approved, the drug could be the first approved treatment for bronchiectasis patients, with a product launch expected in mid-2025. Management expects to commercially launch the drug in Europe and Japan in the first half of 2026.

Apart from bronchiectasis, Insmed is also evaluating brensocatib in the phase IIb BiRCh study in patients with chronic rhinosinusitis without nasal polyps (CRSsNP). A data readout from this study is expected in second-half 2025. Management also intends to initiate a mid-stage study on the drug in hidradenitis suppurativa (HS) indication before 2024-end.

TPIP Study Results Demonstrate INSM’s Pipeline Potential

Management is also evaluating an investigational inhaled formulation of TPIP in separate mid-stage studies for pulmonary hypertension associated with interstitial lung disease (PH-ILD) and pulmonary arterial hypertension (PAH) indications.

In May, Insmed reported positive top-line safety and tolerability data from a mid-stage study evaluating TPIP in PH-ILD indication. Results from the study showed that treatment with TPIP has the potential to prolong the duration of the effect and reduce dose frequency compared with existing inhaled prostanoid therapies.

Management also claimed that a majority of patients (79.3%) who received TPIP reached the maximum dose of 640 micrograms (μg) following five weeks of treatment compared with 100% in the placebo arm. Per management, 640 μg of TPIP dosed one-time daily contains nearly 60% more treprostinil than current market products dosed four times daily.

Based on these results, Insmed plans to start a late-stage study in PH-ILD indication next year. Top-line data from the PAH study is expected in the second half of 2025.

INSM Aligns With FDA on Arikayce’s Confirmatory Study Goal

Earlier this month, INSM announced that it had reached alignment with the FDA on the primary endpoint of the phase III ENCORE study evaluating Arikayce as a potential treatment for newly-infected patients with mycobacterium avium complex (MAC) lung disease. Management expects to report top-line data from this study in the first quarter of 2026.

Arikayce is currently the only marketed drug in the company’s portfolio. The drug is currently approved under the accelerated pathway for treating a limited patient population — refractory MAC lung disease in adult patients with limited or no alternative treatment options.

If the ENCORE study is successful, it could help Insmed significantly expand the drug’s patient population and also convert the accelerated approval to a full one. Management estimates the total addressable market (TAM) for refractory MAC to be around 30,000 patients in the United States, Europe and Japan. If the drug were also approved in the newly-infected patient population, the TAM would increase to around 275,000 patients in the combined three markets. Based on these factors, management expects Arikayce to generate more than a billion dollars in peak sales.

Our Take on INSM

Compared with other stocks in the biotech space, Insmed’s pipeline shows promise. It also has a regular stream of income thanks to Arikayce sales, which puts less strain on the company’s accumulated cash balance of around $1.25 billion (as of June 2024-end). The company also has a significant first-mover advantage in the bronchiectasis space — a market with vast commercial potential. Given the success obtained by Insmed in pipeline development, it could also be eyed as an attractive acquisition target by big pharma.

INSM Zacks Rank

Insmed currently carries a Zacks Rank #3 (Hold).

Insmed, Inc. Price

Insmed, Inc. price | Insmed, Inc. Quote

Our Key Picks Among Biotech Stocks

A couple of better-ranked stocks include Bioventus BVS and Fulcrum Therapeutics FULC, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

In the past 60 days, estimates for Bioventus’ 2024 earnings per share have risen from 27 cents to 40 cents. Estimates for 2025 have increased from 43 cents to 45 cents during the same period. Year to date, shares of Bioventus have surged 89.3%.

BVS’ earnings beat estimates in three of the last four quarters and missed the mark on one occasion. Bioventus delivered a four-quarter average earnings surprise of 102.86%.

In the past 60 days, estimates for Fulcrum Therapeutics’ 2024 loss per share have improved from $1.24 to 48 cents. Estimates for 2025 have improved from $1.71 to $1.51 during the same period. Year to date, Fulcrum Therapeutics’ shares have rallied 44.3%.

Earnings of Fulcrum Therapeutics beat estimates in each of the last four quarters. Fulcrum delivered a four-quarter average earnings surprise of 393.18%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AstraZeneca PLC (AZN) : Free Stock Analysis Report

Insmed, Inc. (INSM) : Free Stock Analysis Report

Fulcrum Therapeutics, Inc. (FULC) : Free Stock Analysis Report

Bioventus Inc. (BVS) : Free Stock Analysis Report