2 Retail Home Furnishing Stocks to Watch Defying Industry Challenges

Despite the Fed’s decision to cut interest rates, consumers remain cautious about jobs and business conditions. This pessimistic approach to future business conditions is concerning for the Zacks Retail-Home Furnishings industry players. Continued investments in e-commerce, high operating expenses and higher raw material costs in the home furnishing market are added headwinds. Nonetheless, consumers’ increasing desire for shopping, efficient cost management, a persistent focus on product innovation, efforts to redesign the supply-chain network and rationalize product offerings, as well as investments in the merchandising of brands and digital marketing should lend support to companies like Williams-Sonoma, Inc. WSM and Fortune Brands Innovations, Inc. FBIN.

Industry Description

The Zacks Retail-Home Furnishings industry comprises retailers offering home furnishing products under various categories. The merchandise assortment includes furniture, garden accessories, framed art, lighting, mirrors, candles, tableware, lamps, picture frames, bathware, accent rugs, artificial floral products, and child and teen furnishing. The industry players also develop, manufacture, market and distribute bedding products. The companies provide home and security products for residential home repair, remodeling, new construction and security applications. They are involved in manufacturing, assembling and selling faucets, accessories, kitchen sinks and waste disposal.

3 Trends Shaping the Future of the Retail-Home Furnishings Industry

Low Consumer Confidence: In September, consumer confidence dropped sharply, with the Conference Board's consumer confidence index falling to 98.7 from 105.6 in August. This is the largest one-month decline since August 2021. Consumers became more pessimistic about the economy, particularly concerning jobs and business conditions. Their views on current business conditions turned negative, and they expressed more concerns about future labor market conditions, business outlook, and income.

The report was released shortly after the Federal Reserve cut interest rates by half a percentage point — the first cut in four years — due to a favorable inflation outlook and concerns about a weakening labor market.

Consumers are adopting a more cautious stance toward their disposable income and appearing to shift toward essentials, which is echoed in the sales report. Furniture and home furnishing store sales declined 0.7% in August 2024 compared to last year.

Stiff Competition: The home furnishing industry is highly competitive, with interior design trade and specialty stores, antique dealers, national and regional home furnishing retailers as well as department stores giving a hard time. Online retailers focused on home furnishing also pose a threat. Competitive product pricing has been eating into margins.

Strong Digital Platform, Product Reinvention & Marketing Moves: The optimization of the supply chain and an improvement in e-commerce channels are expected to drive the top line. E-commerce will continue to play a major role as people find it more comfortable and safer to shop online. Product innovation plays a pivotal role in market share gain in this industry. Companies aim to come up with products and collaborate with celebrated brands and designers to maintain exclusivity. Also, customer experience is being enhanced by innovative marketing techniques, with an emphasis on digital marketing, better merchandising, store remodeling and loyalty programs.

Zacks Industry Rank Indicates Dull Prospects

The Zacks Retail-Home Furnishings industry is a seven-stock group within the broader Zacks Retail-Wholesale sector. The industry currently carries a Zacks Industry Rank #211, which places it in the bottom 16% of more than 250 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates bleak near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

The industry’s positioning in the bottom 50% of the Zacks-ranked industries is a result of a lower earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are gradually losing confidence in this group’s earnings growth potential. Since June 2024, the industry’s earnings estimates for 2024 have decreased to $4.22 per share from $4.31.

Despite the industry’s blurred near-term view, we will present a few stocks that one may consider adding to their portfolio. Before that, it’s worth taking a look at the industry’s shareholder returns and current valuation.

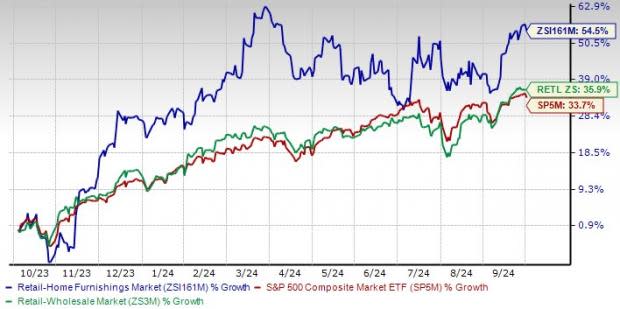

Industry Outperforms the Sector & S&P 500

The Zacks Retail-Home Furnishings industry has outperformed the broader Zacks Retail-Wholesale sector and the Zacks S&P 500 Composite over the past year.

The industry has risen 54.5% compared with the broader sector’s 35.9% growth. The Zacks S&P 500 Composite has gained 33.7% over this period.

One-Year Price Performance

Industry's Current Valuation

On the basis of the forward 12-month price-to-earnings ratio, which is commonly used for valuing retail home furnishing stocks, the industry is currently trading at 17.06 compared with the S&P 500’s 21.56 and the sector’s 23.85.

Over the last five years, the industry has traded as high as 19.44X and as low as 7.15X, with the median being 13.75X, as the chart below shows.

Industry’s P/E Ratio (Forward 12-Month) Versus S&P 500

2 Retail-Home Furnishings Stocks to Watch

We have highlighted two stocks from the industry that are capitalizing on fundamental strengths and have solid growth prospects.

Williams-Sonoma: This is a San Francisco, CA-based multi-channel specialty retailer. The company has been benefiting from its focus on digital initiatives, higher e-commerce penetration and product introductions. Williams-Sonoma is capitalizing on its strategic emphasis on broadening its product range and establishing a sustainable operational framework. By adopting a digital-first approach without exclusively relying on digital-only channels, the company has gained a competitive edge. Its strong e-commerce platform and successful Business-to-Business segment position it for substantial expansion, overcoming ongoing consumer spending challenges. The company’s portfolio of brands serving a range of categories, aesthetics and life stages are tailwinds.

The WSM stock — currently carrying a Zacks Rank #3 (Hold) — has gained 51.1% over the past year. This company surpassed earnings estimates in all the trailing four quarters, the average being 17.4%. It also has a favorable VGM Score of A, with a Value Score of B and a Growth Score of B, making it a potentially interesting investment opportunity. The estimated figure for 2024 indicates 7.5% year-over-year growth. It has a ROE of 51.6%, better than the industry’s 44.3%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: WSM

Fortune Brands Innovations: Based in Deerfield, IL, this company provides home and security products for residential home repair, remodeling, new construction and security applications in the United States and internationally. Although weaker sales in China have been a challenge, Fortune Brands expects continued growth in core and digital businesses, strong margins, and long-term shareholder value through sales growth, margin expansion, and strategic investments. It has been experiencing strong performance in its core businesses, particularly the Outdoors segment and Moen North America, as well as accelerated digital sales. The company has been focusing on an alteration in the cost structure, proficient production planning, protecting margins and improving cash generation. The company has rebranded its entire company, with a business focused on driving accelerated growth in categories through brand and innovation. It has reorganized the company from a decentralized structure with separate businesses to an aligned operating model that prioritizes activities that are key to brand, innovation and channel. These transformative changes will enable Fortune Brands to drive growth in the future.

The FBIN stock has risen 15.1% over the past year. This company, carrying a Zacks Rank #3, surpassed earnings estimates in all the trailing four quarters, the average being 6.5%. The estimated figure for 2024 indicates 9.7% year-over-year growth. It also has a favorable VGM Score of B, with a Value Score of B and a Growth Score of B.

Price and Consensus: FBIN

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Williams-Sonoma, Inc. (WSM) : Free Stock Analysis Report

Fortune Brands Innovations, Inc. (FBIN) : Free Stock Analysis Report